Indian Defence Ecosystem Market Report 2026

Full Strategic Industry Report with Deep Market Insights, SWOT Analysis, and PESTLE Analysis

Author Devanssh Mehta Mode

Executive Summary

India’s defence ecosystem in 2026 has entered a new industrial phase where national security, industrial capability, technological sovereignty, manufacturing competitiveness, and export ambition are increasingly integrated into one strategic framework.

Historically, Indian defence was viewed primarily through military readiness and procurement. The 2026 landscape is fundamentally different. Defence now operates as a strategic economic multiplier influencing aerospace, electronics, shipbuilding, advanced materials, cyber systems, artificial intelligence, semiconductors, manufacturing employment, innovation ecosystems, and geopolitical positioning.

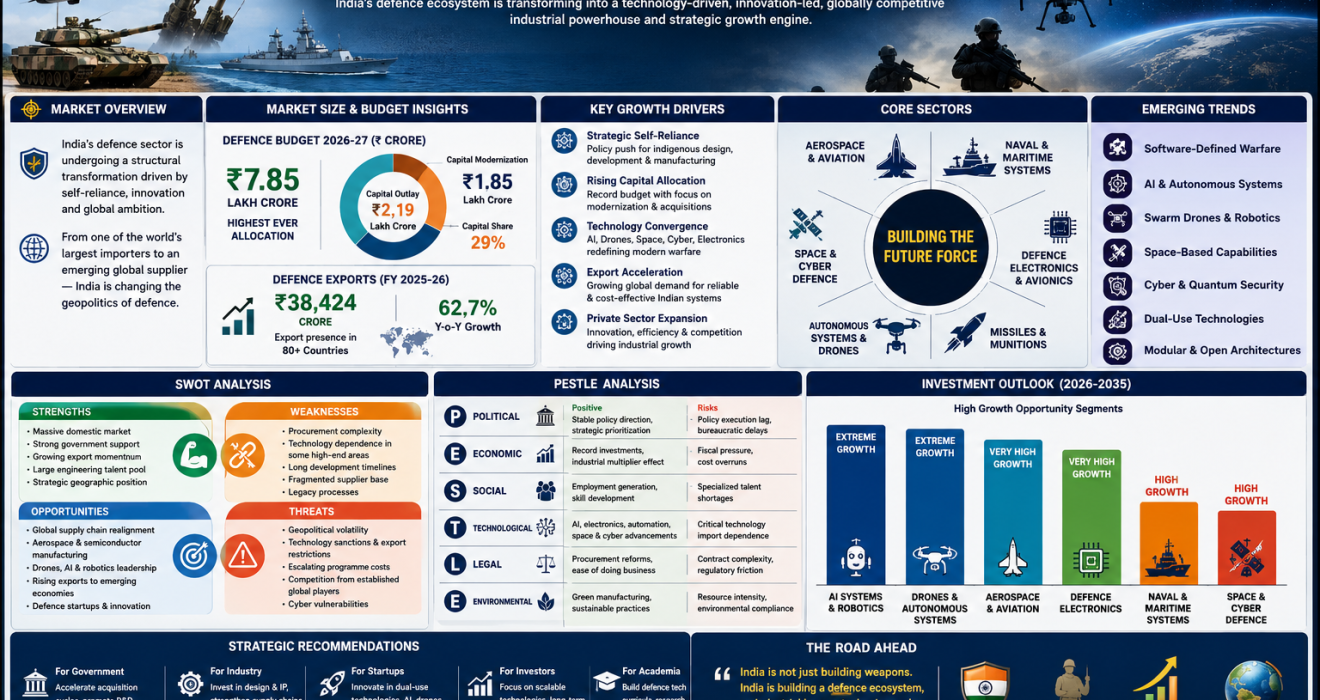

The Union Budget 2026–27 allocated approximately ₹7.85 lakh crore to defence, the highest ever allocation, with capital modernization crossing ₹2.19 lakh crore and approximately ₹1.85 lakh crore dedicated to acquisitions and modernization, signalling accelerated capability building and domestic industrial expansion. (Press Information Bureau)

Simultaneously, India recorded ₹38,424 crore in defence exports in FY 2025–26, representing approximately 62.7% year-on-year growth, demonstrating that India is increasingly transitioning from a defence-importing nation toward a defence-producing and exporting power. (The Times of India)

This report evaluates the structure, economics, industrial dynamics, opportunities, threats, and future outlook of India’s defence ecosystem.

Part I — Strategic Context: The Reinvention of Indian Defence

Modern defence ecosystems globally are no longer military institutions alone.

They have evolved into integrated national capability systems consisting of:

- Industrial manufacturing

- Advanced engineering

- Scientific research

- Strategic logistics

- Export capability

- Innovation ecosystems

- Talent development

- Technology ownership

India’s defence transformation is being driven by five simultaneous transitions:

| Historical Model | Emerging 2026 Model |

|---|---|

| Import dependence | Indigenous production |

| Platform purchase | Platform ownership |

| Public-sector concentration | Mixed public–private ecosystem |

| Security spending | Strategic investment |

| Procurement-led | Innovation-led |

The Indian defence ecosystem increasingly resembles a strategic industrial architecture rather than a conventional ministry-driven procurement model.

Part II — Market Architecture of the Indian Defence Ecosystem

1. Defence Budget and Capital Formation

The Ministry of Defence remains India’s largest central expenditure segment.

Key structural indicators:

- Total defence allocation approximately ₹7.85 lakh crore.

- Capital outlay approximately ₹2.19 lakh crore.

- Capital modernization increase approximately 22%.

- Defence share approximately 14.7% of central expenditure.

- Capital allocation approaching 29% of total defence spending. (MP-IDSA)

This budget composition signals a shift from sustaining forces toward creating future combat capability.

2. Defence Industrial Segments

Aerospace and Aviation

India increasingly prioritizes:

- Combat aircraft

- Transport systems

- Engines

- Aerospace integration

- Avionics

Aircraft and aero-engine allocation exceeded ₹63,000 crore in Budget 2026, reflecting long-term air power modernization priorities. (The Economic Times)

Naval and Maritime Systems

Growth areas:

- Indigenous shipbuilding

- Maritime surveillance

- Undersea capabilities

- Strategic sea-lane protection

Naval fleet modernization continues to receive dedicated capital expansion. (The Economic Times)

Defence Electronics

Electronics increasingly define battlefield superiority.

Strategic areas:

- Electronic warfare

- Radar

- Secure communications

- Sensors

- Embedded systems

- Battlefield networking

Electronics may become India’s largest defence value segment over the next decade.

Autonomous Systems and Drones

India’s emerging battlefield doctrine increasingly emphasizes:

- Precision strike

- Autonomous surveillance

- Swarm intelligence

- Tactical AI

Drone systems are becoming one of the fastest-growing subsegments.

Space and Cyber Defence

Strategic competition increasingly extends beyond geography.

Emerging domains:

- Space monitoring

- Satellite resilience

- Cyber defence

- Data dominance

- Quantum security

Part III — Market Growth Drivers

Driver 1: Strategic Self-Reliance

Domestic procurement and local production increasingly dominate acquisition policy.

Industrial self-reliance is becoming synonymous with national resilience.

Driver 2: Export Acceleration

Defence exports reached record levels and are increasingly supported by both public and private manufacturing ecosystems. Government ambitions target approximately ₹50,000 crore exports by 2029. (Press Information Bureau)

Driver 3: Technology Convergence

Defence increasingly overlaps with:

- AI

- Robotics

- Materials science

- Semiconductor systems

- Space technologies

Driver 4: Private Sector Expansion

Private participation is improving:

- Manufacturing velocity

- Cost competitiveness

- Innovation cycles

Driver 5: Infrastructure-Led Industrial Growth

Record national infrastructure spending indirectly strengthens defence logistics and manufacturing ecosystems. (Reuters)

Part IV — Defence Value Chain Analysis

Upstream Layer

Inputs:

- Metals

- Electronics

- Sensors

- Components

- Propulsion

Midstream Layer

Transformation:

- Manufacturing

- Systems integration

- Testing

Downstream Layer

Outputs:

- Platforms

- Services

- Maintenance

- Exports

Strategic Support Layer

- Academia

- R&D

- Policy

- Financing

- Workforce

The future competitive advantage lies not in platform assembly but in controlling intellectual property and systems integration.

Part V — Emerging Trends Defining Indian Defence 2026–2035

Trend 1 — Software-Defined Warfare

Future defence value shifts toward:

- Algorithms

- Battlefield intelligence

- Data systems

Trend 2 — Defence-as-Manufacturing

Defence increasingly behaves like advanced manufacturing.

Trend 3 — Export Diplomacy

Exports increasingly influence geopolitical relationships.

Trend 4 — Modular Platforms

Flexibility becomes more valuable than platform size.

Trend 5 — Dual-Use Technology Growth

Commercial technologies increasingly enter defence applications.

Part VI — SWOT Analysis of Indian Defence Ecosystem (2026)

Strengths

Massive Domestic Market

One of the world’s largest modernization pipelines.

Government Commitment

Record budget allocation supports execution. (Press Information Bureau)

Export Momentum

Record export growth validates industrial capability. (The Times of India)

Large Engineering Talent Base

Strategic Geography

Weaknesses

Procurement Complexity

Limited Indigenous Capability in Select High-End Technologies

Long Development Timelines

Fragmented Supplier Networks

Legacy Institutional Structures

Opportunities

Global Supply Chain Realignment

Aerospace Manufacturing Leadership

Drone and AI Platforms

Semiconductor Integration

Defence Technology Startups

Export Market Expansion

Threats

Regional Geopolitical Volatility

Technology Restrictions

Escalating Program Costs

Global Competitive Pressure

Cyber Vulnerabilities

SWOT Strategic Interpretation

India’s greatest strategic challenge is no longer capability creation.

It is execution speed, scale discipline, and technology depth.

Part VII — PESTLE Analysis of Indian Defence Market

Political Factors

Positive:

- Stable strategic direction

- Long-term defence prioritization

Risks:

- Policy execution lag

Impact:

High

Economic Factors

Positive:

- Record public investment

- Industrial multiplier effect

Risks:

- Fiscal pressure

Impact:

Very High

Social Factors

Positive:

- Employment generation

- Skill development

Risks:

- Specialized talent shortages

Impact:

Medium–High

Technological Factors

Positive:

- AI

- Automation

- Electronics

Risks:

- Critical technology imports

Impact:

Extreme

Legal Factors

Positive:

- Procurement reform

Risks:

- Contract complexity

Impact:

Medium

Environmental Factors

Positive:

- Sustainable manufacturing

Risks:

- Resource intensity

Impact:

Moderate

Part VIII — Competitive Landscape Outlook

Future competitive advantage will likely emerge from companies and institutions capable of controlling:

- Design

- Electronics

- Software

- Integration

- Export ecosystems

Winning characteristics:

✓ Faster innovation

✓ Indigenous IP

✓ Export readiness

✓ Modular engineering

✓ Capital efficiency

Part IX — Investment Outlook (2026–2035)

High-opportunity segments:

| Segment | Outlook |

|---|---|

| Defence Electronics | Extreme Growth |

| Aerospace | Very High |

| AI Systems | Extreme Growth |

| Drones | Extreme Growth |

| Space Defence | High |

| Cybersecurity | Extreme Growth |

| Naval Systems | High |

Part X — Strategic Recommendations

Government

- Accelerate procurement cycles

- Expand advanced R&D

Industry

- Build platform ownership

- Invest in deep engineering

Academia

- Create defence innovation clusters

Investors

- Focus on scalable technologies

Startups

- Target dual-use technologies

Final Conclusion

The Indian defence ecosystem of 2026 represents far more than military modernization.

It is becoming a national industrial transformation project.

Its future success will not be determined merely by budget size or procurement volumes—but by how effectively India converts expenditure into sovereign technology, converts technology into manufacturing strength, and converts manufacturing strength into global influence.

If execution remains disciplined and innovation intensity continues, India’s defence industry may become one of the defining strategic growth stories of the coming decade.