Indian Diabetic Market Size Analysis Report (2026)

A Comprehensive Strategic Assessment of India’s Diabetes Economy

By Author Devanssh Mehta

Executive Summary

India has transitioned from being described merely as the “diabetes capital of the world” to becoming one of the largest diabetes healthcare economies globally. Diabetes in India is no longer only a chronic disease burden—it is now a multidimensional economic ecosystem involving pharmaceuticals, insulin, diagnostics, devices, preventive healthcare, insurance, digital therapeutics, nutrition, and long-term chronic care. (EUCLID School of Global Health)

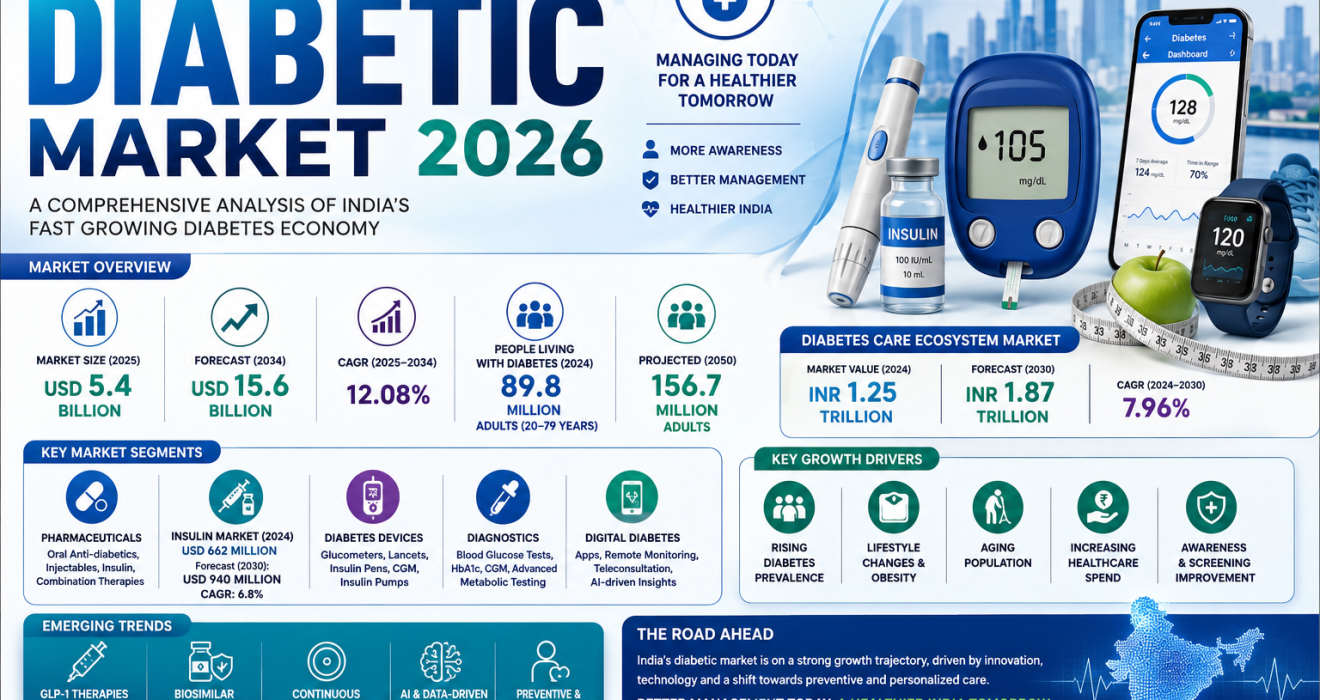

Recent industry estimates suggest the Indian diabetes market reached approximately USD 5.4 billion in 2025 and may expand to nearly USD 15.6 billion by 2034 at a CAGR of approximately 12.08%. (MarketResearch.com)

At the broader diabetes-care ecosystem level (including devices, diagnostics, services, monitoring, and treatment), the market was estimated at approximately INR 1.25 trillion in 2024 and is projected to reach INR 1.87 trillion by 2030. (Business Wire)

India is estimated to have approximately 89.8 million adults (20–79 years) living with diabetes in 2024, with projections indicating continued expansion toward 156.7 million by 2050 if current trajectories persist. (IMARC Group)

This report presents a detailed strategic analysis of:

- Market size and valuation

- Disease burden and epidemiology

- Pharmaceutical opportunities

- Device and digital market evolution

- Competitive ecosystem

- SWOT and PESTLE analysis

- Future investment outlook

1. Introduction: Diabetes Has Become an Economic Sector

Historically, India’s healthcare growth was driven by infectious diseases and acute care.

Today, chronic diseases dominate.

Among them, diabetes occupies a unique position because:

- treatment is lifelong,

- diagnosis is expanding,

- monitoring is recurring,

- complications create secondary markets.

The diabetic market today includes:

Prevention

↓

Diagnostics

↓

Drug therapy

↓

Insulin

↓

Monitoring devices

↓

Hospital services

↓

Digital monitoring

↓

Complication management

This creates a continuous economic cycle.

2. Market Size of Diabetes Industry in India

Because different analysts define the market differently, multiple estimates coexist.

A. Overall Diabetes Market

| Metric | Value |

|---|---|

| Market Size (2025) | USD 5.4 Billion |

| Forecast (2034) | USD 15.6 Billion |

| CAGR | 12.08% |

B. Diabetes Care Ecosystem

| Metric | Value |

|---|---|

| Market Value (2024) | INR 1.25 Trillion |

| Forecast (2030) | INR 1.87 Trillion |

| CAGR | 7.96% |

C. Diabetes Drugs Segment

| Metric | Estimate |

|---|---|

| Market (2025) | USD 1.76 Billion |

| Forecast (2031) | USD 2.16 Billion |

3. Epidemiological Foundation of Growth

The diabetic market exists because of unprecedented disease expansion.

Major growth drivers include:

Demographic

- Aging population

- Increased longevity

Lifestyle

- Sedentary work

- Reduced activity

- Calorie excess

Metabolic

- Obesity

- Insulin resistance

Environmental

- Urbanization

- Stress

India crossed approximately 100 million diagnosed diabetes cases in recent estimates, making it among the largest diabetes populations globally. (Yahoo Finance)

4. Disease Segmentation and Commercial Structure

Type 1 Diabetes

Smaller volume.

High dependence on:

- insulin

- CGM

- specialty care

Type 2 Diabetes

Largest market segment.

Industry estimates suggest Type-2 contributes approximately 78% market share in India. (The Report Cube)

Drivers:

- obesity

- genetics

- urban lifestyle

Gestational Diabetes

Rapidly emerging category.

Important growth area because of:

- maternal screening

- preventive interventions

5. Pharmaceutical Market Analysis

Indian diabetes pharmacotherapy has evolved through four generations.

Generation 1

Metformin

Generation 2

Sulfonylureas

Generation 3

DPP-4 inhibitors

Generation 4

SGLT-2 and GLP-1

Current growth increasingly comes from premium and combination therapies. Recent pharmaceutical tracking indicates accelerated adoption of newer drug classes including GLP-1 therapies. (The Times of India)

6. Insulin Market Analysis

Insulin remains the backbone of advanced diabetes care.

India insulin market:

| Metric | Value |

|---|---|

| Revenue (2024) | USD 662 Million |

| Forecast (2030) | USD 940 Million |

| CAGR | 6.8% |

Major trends:

- biosimilar insulin

- analog adoption

- affordability programs

Insulin analog currently contributes the largest revenue share. (Grand View Research)

7. Diabetes Device Economy

Devices increasingly determine patient engagement.

Major categories:

- glucometers

- lancets

- insulin pens

- CGM

- pumps

India’s lancets market alone expanded to approximately USD 135.8 million in 2025 with long-term double-digit growth expectations. (Towards Healthcare)

Device expansion is driven by:

- self-monitoring

- home care

- telemedicine

8. Rise of Digital Diabetes

Digital diabetes management is becoming an independent business segment.

Growth pillars:

Remote Monitoring

Mobile Apps

AI-Assisted Management

Tele-Endocrinology

Digitalization improves:

- adherence

- follow-up

- early intervention

9. Diagnostic Market Transformation

Testing demand now extends beyond fasting glucose.

Growth areas:

- HbA1c

- CGM

- molecular risk profiling

- metabolic assessment

Diagnostics increasingly function as recurring revenue channels.

10. Retail Pharmacy and Distribution Dynamics

Distribution channels:

Retail Pharmacies

Largest channel.

Retail contributes approximately 57% of diabetes market distribution value. (IMARC Group)

Hospitals

Growth driver:

- complex diabetes

E-pharmacy

Emerging channel.

Drivers:

- convenience

- subscription models

11. Competitive Landscape

Market participants broadly include:

Global Leaders

- insulin innovators

- device companies

Indian Companies

- generics

- biosimilars

- chronic therapy portfolios

Strategic competition increasingly focuses on:

- affordability

- adherence

- combination therapy

12. Emerging GLP-1 Economy

One of the most important developments in India.

Premium diabetes therapies have begun reshaping market economics.

Recent market commentary indicates rapid expansion in GLP-1 use while remaining a smaller proportion of total diabetes volume. (The Times of India)

Recent launches and upcoming generic competition are expected to intensify the segment. (Reuters)

13. Healthcare Infrastructure Impact

Diabetes expansion is influencing:

- clinics

- diagnostics

- hospital OPDs

- specialist demand

Challenges remain:

- late diagnosis

- inconsistent follow-up

- rural access gaps

14. Economics of Diabetes

Direct costs:

- medicines

- devices

- diagnostics

Indirect costs:

- lost productivity

- absenteeism

- complications

Macro-economic consequences include:

- workforce reduction

- insurance burden

- chronic healthcare inflation

15. Investment Landscape

Highest Opportunity Areas:

★★★★★ Digital Diabetes

★★★★★ Devices & CGM

★★★★★ Biosimilar Insulin

★★★★★ Diabetes Diagnostics

★★★★ Chronic Care Platforms

★★★★ Preventive Nutrition

16. SWOT Analysis

Strengths

- Massive patient base

- Strong pharmaceutical manufacturing

- Growing diagnostics

Weaknesses

- High out-of-pocket spending

- Rural access limitations

Opportunities

- AI healthcare

- Precision diabetes

- Export markets

Threats

- Rising obesity

- premium treatment affordability

- counterfeit medicine risks

Authorities have recently acted against suspected counterfeit diabetes products, highlighting supply-chain vigilance needs. (Reuters)

17. PESTLE Analysis

Political

Expansion of healthcare programs.

Economic

Growing healthcare spending.

Social

Urban lifestyle changes.

Technological

Digital monitoring.

Legal

Regulatory strengthening.

Environmental

Lifestyle and pollution interaction.

18. Future Outlook to 2035

The Indian diabetic market will likely move through three major transitions:

Phase I

Drug expansion

Phase II

Digital diabetes ecosystems

Phase III

Predictive and precision diabetes

Expected dominant growth engines:

- GLP-1 therapies

- biosimilar insulin

- home monitoring

- AI-enabled chronic care

- preventive diagnostics

Long-term forecasts across major market models consistently indicate sustained expansion through 2034–2035. (Market Research Future)

Conclusion

India’s diabetic market is no longer simply a pharmaceutical category.

It has evolved into a full chronic disease economy integrating treatment, diagnostics, devices, technology, insurance, and behavioral healthcare.

The next decade will determine whether India remains primarily a large consumer market—or becomes a global leader in affordable diabetes innovation.

The winners of India’s diabetic economy will not merely manufacture medicines.

They will create integrated ecosystems that prevent disease, improve adherence, reduce complications, and make long-term care economically sustainable.